The Real Story in ADCs: Market Shifts, Manufacturing Chokepoints, and the Race for Top Oncology Talent

Byron Fitzgerald

Founder, ProGen Search

The global biopharmaceutical sector has entered a highly accelerated, structural phase of oncology asset consolidation, driven almost entirely by the unprecedented maturation of the Antibody-Drug Conjugate (ADC) modality. With over 600 programs currently active in the global clinical pipeline, the market is no longer simply validating the science behind ADCs; it is engaged in a brutal war for execution, scale, and commercial dominance.

For companies building teams in this space, the stakes have never been higher. The aggregate market size for ADCs, previously valued at $16.53 billion in 2025, is accelerating on a trajectory toward an estimated $46.95 billion by 2030. However, the talent required to capture this value has fundamentally changed. If you are hiring in ADCs using the traditional biologics playbook, you are fundamentally mispricing the sector. The winners in the 2026 market will not be defined merely by who discovers the next novel target, but by who controls the chemistry, locks down the manufacturing, and recruits the elite executive leadership capable of navigating a hyper-complex global supply chain.

As a premier life sciences executive search firm, Progen Search partners with biotech innovators to build the leadership teams driving this revolution. Here is a deep dive into the structural changes defining the ADC market today, and what they mean for your next critical executive hire.

The Innovation Axis Flipped: The Geographic "Barbell" Paradigm

For decades, the prevailing narrative dictated that Western laboratories generated first-in-class innovation, while Asian markets served primarily as high-volume manufacturing hubs. In the ADC sector, this historical flow of pharmaceutical technology has definitively inverted. The center of gravity for preclinical and early-stage clinical innovation has firmly shifted toward Greater China.

The data is unambiguous: in 2025, Chinese originators accounted for nearly 90% of global ADC out-licensing, driving a record $137.7 billion in cross-border deals. Average upfront deal values surged by 230%, proving that Western pharma is no longer utilizing China as a "bargain basement". Instead, a "Barbell Paradigm" has emerged. Western Big Pharma has largely transitioned into a well-funded commercial distribution arm, using "Territory Hybrid" deals to externalize and offload early-stage clinical risk to the East.

Under these Territory Hybrid structures, the Chinese biotechnology originator retains the clinical and commercial rights for Greater China, while out-licensing the "Rest of World" (ROW) rights to a Western pharmaceutical partner. We are seeing this executed at massive scale:

RemeGen Biosciences secured a $5.6 billion exclusive oncology agreement with AbbVie.

MediLink Therapeutics executed a $570 million global licensing agreement with Roche for a B7-H3 targeting asset.

Kelun-Biotech is supplying the highly potent TROP2 ADC, MK-2870, to power Merck's multi-billion-dollar portfolio transition.

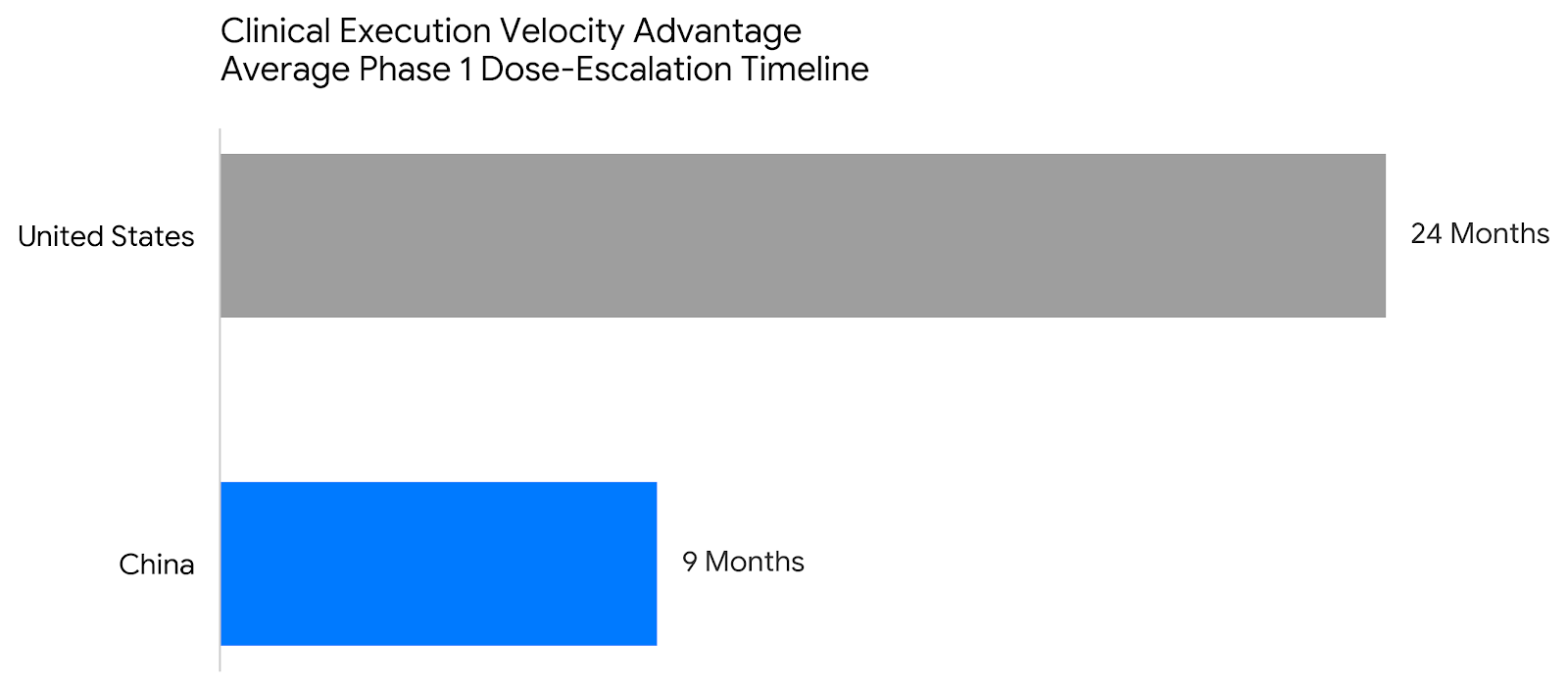

Chinese biotechs are supercharged by 30-day IND approvals, frequently completing Phase 1 dose-escalation trials in just 9 months - compared to a 24-month average in the United States. However, this Eastern speed must be matched with Western regulatory rigor. The FDA strictly enforces a requirement that at least 20% of a clinical trial's patient enrollment must occur within the United States for a drug to receive domestic approval, aggressively pushing back against the reliance on single-country clinical packages.

The ADC Executive Search Implication: This geographic bifurcation has created an immense demand for specialized Business Development (BD) and Global Alliance Management executives. Hiring in ADCs today requires leaders who possess deep cross-border fluency, an understanding of complex milestone-stacking in licensing deals, and the ability to bridge Eastern clinical velocity with strict Western regulatory mandates (FDA/EMA). A specialized headhunter for ADCs is critical to identifying talent capable of managing these high-stakes, multi-billion-dollar global alliances.

Chemistry is Eating Biology: The Death of the "Biological Premium"

Capital allocators are still using a legacy playbook, paying massive valuation premiums for "first-in-class" biological target novelty. They fundamentally misunderstand that a modern ADC is a highly engineered, modular chemical vehicle, where the antibody acts merely as an interchangeable, programmable delivery chassis.

In 2026, the true economic moats are defined by proprietary linker-payload chemistry. A highly novel antibody paired with an unstable linker or a generic toxin will inevitably fail in Phase 2 due to dose-limiting toxicities. Conversely, a well-characterized, biologically unoriginal antibody paired with a breakthrough conditionally cleavable linker and a highly selective payload will generate massive blockbuster economics.

This "Chemistry Flip" is driving massive strategic acquisitions:

Otsuka Pharmaceutical's $400 million acquisition of Araris Biotech was driven entirely by preclinical data for a highly hydrophilic, triple-payload peptide linker - not a novel target.

Eli Lilly acquired Mablink to secure advanced linker technologies, revealing that its internal FRα-directed ADC achieved a 40% response rate in patients with extremely low antigen expression.

Tubulis secured a massive €308 million Series C financing to advance highly stable, site-specific conjugation methodologies engineered to eliminate premature payload shedding.

Lonza’s Advanced Synthesis bioconjugate division, driven by its integration of Synaffix's site-specific platforms, reported an exceptional 22.4% constant exchange rate sales growth.

The industry is aggressively pivoting toward next-generation architectures, including dual-payload and bispecific ADCs. Chinese developers currently contribute 54% of all bispecific ADCs and 38% of all dual-payload ADCs in global development. Akeso, for example, is advancing a first-in-class Trop2/Nectin4 bispecific ADC to proactively defeat acquired tumor resistance.

The ADC Executive Search Implication:

The war for talent has migrated from the biology lab to the chemistry department. Biotech executive recruiters are seeing unprecedented demand for elite Bioconjugation Scientists, Medicinal Chemists, and Preclinical R&D Heads who understand how to actively widen the therapeutic window using hydrophilic linkers and topoisomerase I inhibitors. When hiring in ADCs, securing a Chief Scientific Officer (CSO) who understands that chemistry is the primary value driver is non-negotiable.

The Manufacturing Chokepoint: Capacity as a Valuation Premium

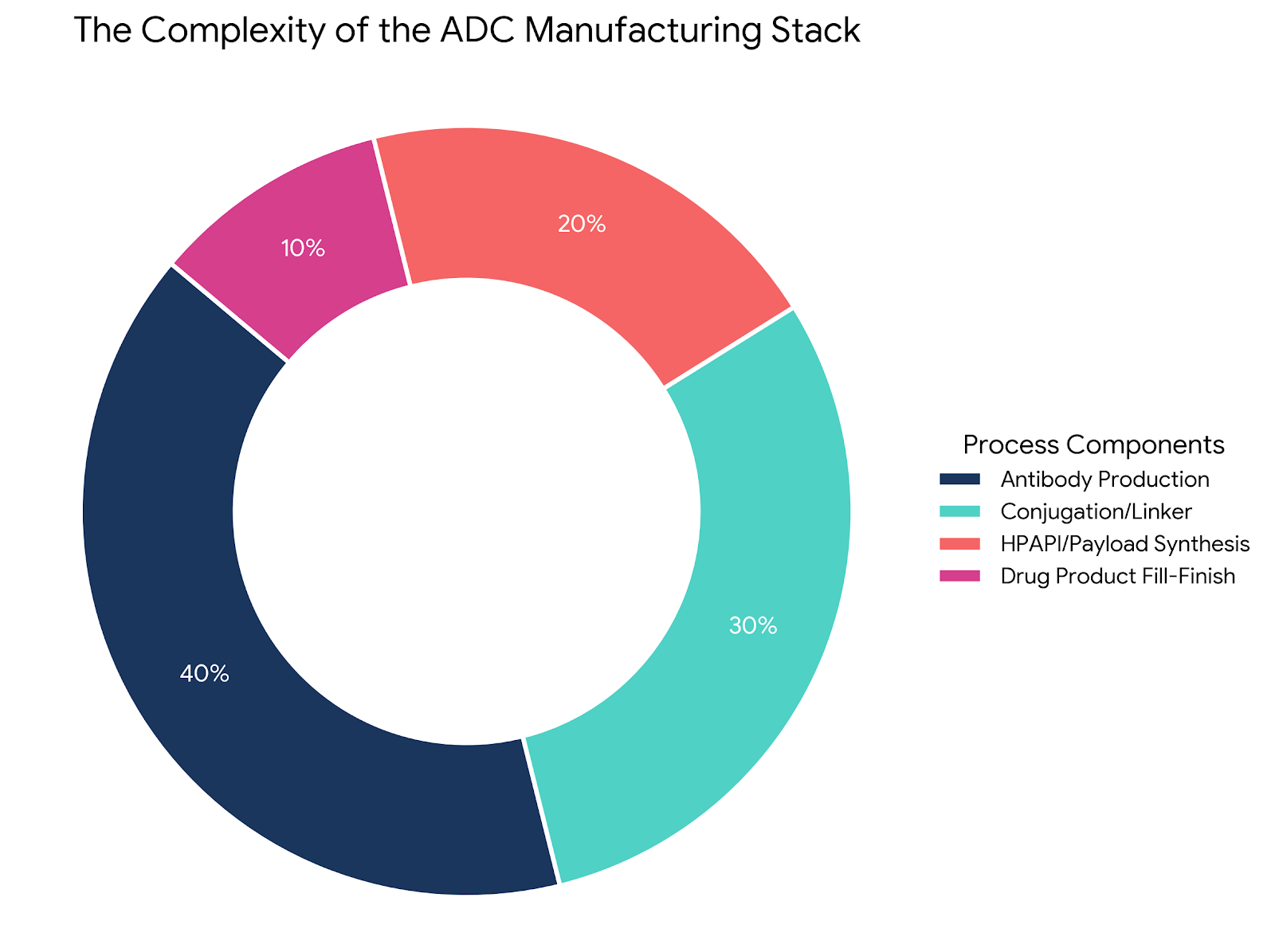

A clinical-stage ADC with flawless Phase 2 data is functionally worthless if it cannot secure Western-based GMP containment capacity for commercial scale-up. The global contract manufacturing (CDMO) sector is currently masking a catastrophic execution gap between "paper capacity" (steel bioreactors) and actual aseptic fill-finish capability.

Approximately 40% of the active ADC development programs originate from small-to-midsize biotechnology firms that structurally lack the capital-intensive infrastructure required to manage high-potency active pharmaceutical ingredients (HPAPIs). Because ADCs combine delicate proteins with highly toxic small molecules, they cannot undergo terminal sterilization; they require flawless aseptic lyophilization under extreme OEB 5/6 containment. The severe late-2025 FDA Warning Letter issued to Catalent’s Bloomington facility - citing mammalian hair in vials and catastrophic Quality Unit failures - exposed exactly how fragile this sterile fill-finish process is.

Compounding this technical bottleneck is the legislative hammer of the U.S. BIOSECURE Act. Mandating the decoupling of US supply chains from designated Chinese entities by 2032, the Act is forcing Western biopharma to aggressively reshore their manufacturing networks.

WuXi XDC reported a massive $1.49 billion backlog, but is heavily reliant on the launch of its new Singapore facility to maintain Western clientele amid geopolitical headwinds.

Samsung Biologics acquired a $280 million facility in Maryland to establish a secure, domestic US supply chain.

Lonza is commanding massive premiums because its fully integrated, end-to-end model bypasses the catastrophic logistical friction of moving highly toxic intermediates between disparate corporate entities.

The ADC Executive Search Implication: Capital markets are quietly applying a massive "manufacturing penalty" to biotechs that do not control their physical supply chain. As an executive search company, Progen Search is currently fielding urgent mandates for apex Supply Chain VPs, Chemistry, Manufacturing, and Controls (CMC) Executives, and Quality Assurance (QA) leaders. True CDMO manufacturing leaders who have successfully navigated FDA audits for aseptic lyophilization are the rarest and most valuable assets in the current talent pool.

The Clinical Battlefield: Overall Survival and the Toxicity Ceiling

In the highly contested oncology market, Progression-Free Survival (PFS) is no longer enough to secure dominance; if a highly potent ADC doesn't definitively extend a patient's life, the systemic toxicity burden cannot be justified. Overall Survival (OS) is the new regulatory baseline.

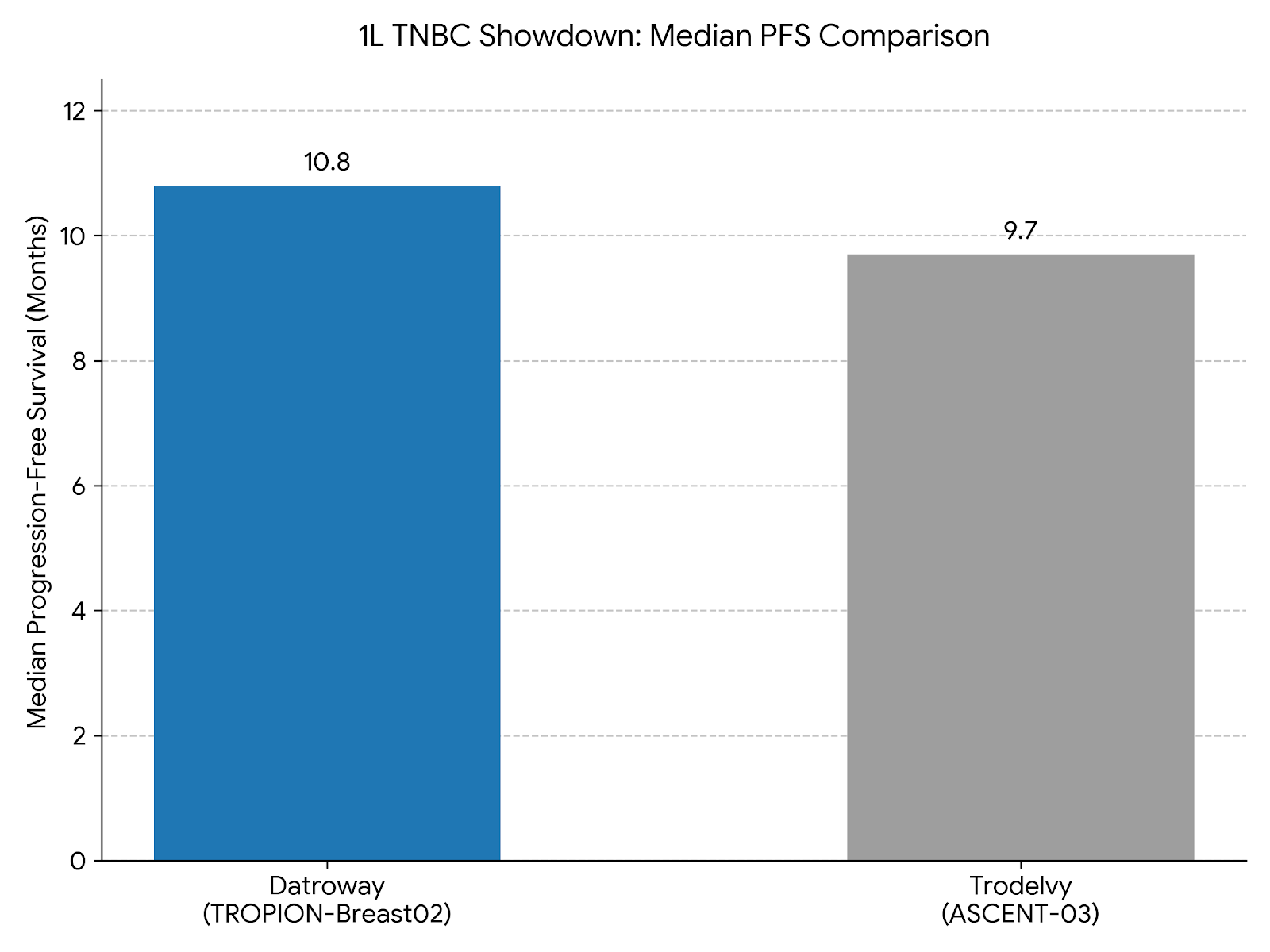

This was definitively proven at the ESMO 2025 Congress in the first-line (1L) metastatic triple-negative breast cancer (mTNBC) setting. AstraZeneca and Daiichi Sankyo’s Datroway (Dato-DXd) seized the market from Gilead's Trodelvy by delivering a definitive 21% reduction in the risk of death (OS win) with zero treatment-related fatalities. Conversely, while Trodelvy demonstrated a strong PFS benefit, it failed to achieve a statistically significant OS win at the time of presentation and reported six treatment-related deaths due to infection, leaving it highly vulnerable.

Furthermore, developers are violently hitting a strict toxicity ceiling. The FDA placed a partial clinical hold on the Phase III trial for Merck and Daiichi Sankyo's ifinatamab deruxtecan (I-DXd) in small cell lung cancer following a higher-than-anticipated incidence of Grade 5 (fatal) interstitial lung disease (ILD) events. Merck and Daiichi were also forced to voluntarily withdraw their BLA for HER3-DXd in EGFR-mutated NSCLC specifically because it failed to prove an OS benefit, despite a prior PFS win.

The market is realizing that you cannot simply staple a topoisomerase I inhibitor to any antibody and expect universal success. Commercial success is now strictly gated by advanced predictive toxicology and precise patient stratification via companion diagnostics.

The ADC Executive Search Implication: Biopharmaceutical developers treating companion diagnostics as a post-Phase 2 afterthought are walking directly into a regulatory buzzsaw. Hiring in ADCs requires securing elite Chief Medical Officers (CMOs), Translational Medicine Heads, and Biomarker Leads who know how to design trials that capture definitive OS endpoints. Oncology leadership talent must now encompass deep expertise in non-animal predictive toxicology and adaptive trial designs to prevent catastrophic late-stage clinical holds.

Building the ADC Dream Team with Progen Search

The ADC sector has formally decoupled from the traditional rules of biologic drug development. The winners in 2026 and beyond will not be the companies that simply outspend their rivals on biological discovery; they will be the operators who engineer superior chemical architectures, legally lock down end-to-end domestic manufacturing slots, and execute their clinical trials with absolute precision.

Building a company capable of this requires a specialized approach to talent acquisition. Generalist biotech executive recruiters frequently lack the technical fluency to distinguish between a traditional biologics manufacturing leader and an executive who has actually scaled OEB 5/6 containment facilities.

At Progen Search, we specialize deeply in life sciences executive search. We understand the nuanced difference between hiring a biologist to find a target and hiring a bioconjugation chemist to build a moat. Whether you need a cross-border BD executive to structure a Territory Hybrid deal, a CMC leader to navigate the BIOSECURE Act, or a CMO to drive an Overall Survival clinical endpoint, we possess the network and the industry intelligence to deliver apex oncology leadership talent.

The question isn't whether ADCs work. It's whether your executive team has the capability to deliver one to the market.

Byron Fitzgerald is the Founder of ProGen Search, a specialist executive search and strategic advisory firm focused on biopharmaceutical manufacturing, complex modalities within Life Sciences, CDMO strategy, and leadership capital. For more on how supply architecture shifts are reshaping leadership requirements in radiopharma, contact byron.fitzgerald@progensearch.com or visit progensearch.com.

You can book a call directly, here.